Tax season usually feels like a collective migraine for about 160 million Americans. You sit there, staring at a W-2 or a messy pile of 1099s, wondering where the money actually goes and, more importantly, if you’re the only one actually footing the bill. Honestly, the conversation around who pays taxes in the us is usually a mess of political shouting matches and half-baked TikTok financial advice. People love to say the rich pay nothing, while others claim the bottom half are "takers." The reality is way more nuanced, a bit frustrating, and deeply tied to how the IRS defines "income" versus "wealth."

The US tax system is a progressive beast. It’s designed so that as you earn more, the percentage you give back climbs. At least, that’s the theory. In practice, the burden of funding the federal government—everything from the military to the person processing your passport—falls on a surprisingly small group of people.

The Top 1% and the Heavy Lifting

If you look at the raw data from the IRS Statistics of Income division, the numbers are kind of staggering. The top 1% of earners in the United States—people making roughly $680,000 or more annually—actually pay about 45.8% of all federal individual income taxes. Think about that for a second. Less than a million households are responsible for nearly half of the income tax revenue that keeps the country running.

It hasn't always been this skewed. Back in 2001, that same group paid about 33%. The shift isn't necessarily because tax rates went through the roof; it’s because the concentration of income at the very top has exploded. When we talk about who pays taxes in the us, we’re really talking about a system that leans heavily on high earners.

But wait. There’s a massive "but" here.

While the top 1% pay the most in total dollars, their effective tax rate—the actual percentage of their total wealth or even their total income they pay—is often lower than a surgeon making $500,000. Why? Capital gains. If you make your money through a paycheck, the IRS hits you with ordinary income rates that can top out at 37%. If you make your money by sitting back and watching your stocks grow, you’re often paying a flat 15% or 20%. This is the "Buffett Rule" territory, named after Warren Buffett’s famous observation that he pays a lower tax rate than his secretary. It’s totally legal. It’s also why people get so fired up about tax fairness.

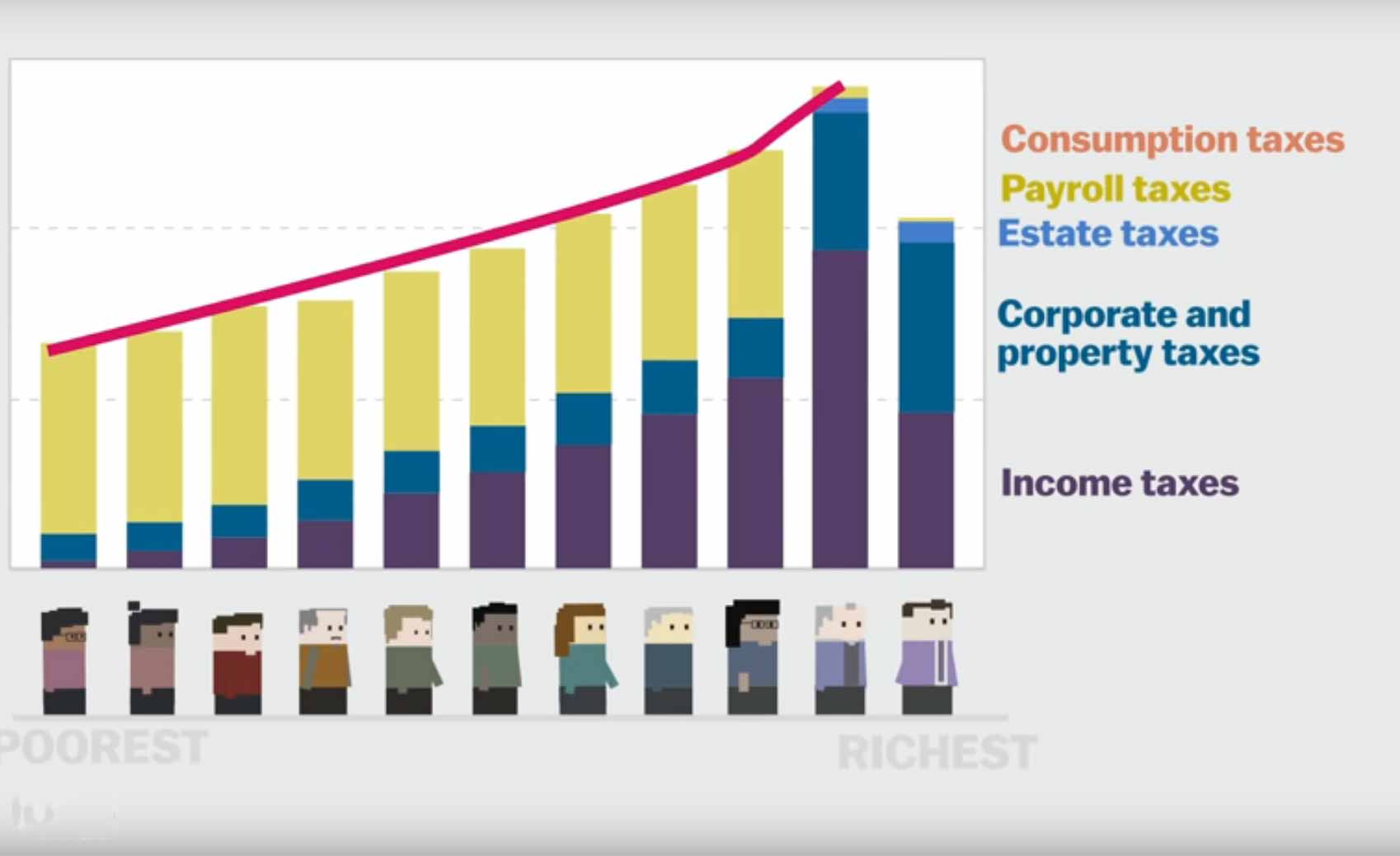

The Missing Middle and the Bottom 50%

Then you have the other side of the coin. There is a persistent myth that half of Americans pay "no taxes." This is technically true for federal income tax, but it’s a massive oversimplification that ignores how most people actually experience the drain on their bank accounts.

According to the Tax Foundation, about 40% to 47% of Americans have a $0 or negative federal income tax liability after deductions and credits like the Child Tax Credit (CTC) or the Earned Income Tax Credit (EITC). But don't think they’re getting a free ride. If you’ve ever looked at a pay stub, you’ve seen those FICA deductions. That’s Social Security and Medicare.

Payroll taxes are regressive. They hit the first dollar you earn. Even if you don't owe a cent in income tax at the end of the year, you've likely been paying 7.65% of your wages into the system all year long (and your employer doubled that). For a vast majority of lower and middle-income workers, payroll taxes are actually a bigger financial hit than income taxes.

Corporate America’s Share of the Pie

We can’t talk about who pays taxes in the us without mentioning corporations. This is where things get murky. You’ve probably seen the headlines: "Company X made $10 billion and paid $0 in taxes." It sounds like a heist. Sometimes, it’s just the way the tax code is built to encourage specific behaviors.

Take Amazon or Tesla. For years, they utilized R&D tax credits and "carryforward" losses. Basically, if a company loses money for five years while building a massive infrastructure, the IRS lets them use those losses to offset profits in the years they finally become profitable.

- Corporate tax revenue accounts for only about 7% to 10% of total federal revenue.

- In the 1950s, that number was closer to 30%.

- The 2017 Tax Cuts and Jobs Act slashed the statutory corporate rate from 35% to 21%.

Most experts, like those at the Brookings Institution, point out that even when corporations pay, the "incidence" of the tax—who actually feels the pain—is split. Some of it comes out of shareholder dividends, but some of it is passed down to workers in the form of lower wages or to consumers through higher prices. It’s a shell game.

The Self-Employed Struggle

If you’re a freelancer or a small business owner, you’re in a unique, and often painful, category of people who pay taxes in the us. You get hit with the "Self-Employment Tax."

When you work for a boss, they pay half of your Social Security and Medicare taxes. When you are the boss, you pay both halves. That’s 15.3% right off the top before you even get to income tax. It’s why so many independent contractors feel like they’re drowning even when they’re making "good" money. You aren't just a taxpayer; you're a tax collector and a tax funder all in one.

High-Tax States vs. Low-Tax States

The federal government isn't the only one with its hand in your pocket. Where you live radically changes your total tax profile.

In California or New York, a high earner might see a combined marginal tax rate (federal + state) north of 50%. Meanwhile, in Florida, Texas, or Washington, there is no state income tax. But—and there’s always a but—those states have to get their money from somewhere. Texas has some of the highest property taxes in the country. Washington relies heavily on sales tax, which hits lower-income people much harder because they spend a larger percentage of their earnings on basic goods.

The Wealth Gap and the "Invisible" Taxpayer

There is a group of people who pay almost nothing relative to their net worth: the ultra-wealthy who don't "realize" their gains. If you own $100 million in Apple stock and it goes up to $200 million, you have $100 million in "unrealized gains." In the eyes of the IRS, you haven't made a dime.

Wealthy individuals often live off loans. They take a low-interest loan against their stock portfolio. Since loan proceeds aren't income, they don't pay taxes on that money. They spend, they live large, and the tax bill never comes due until the assets are sold—or, if they hold them until death, the "step-up in basis" rule can potentially wipe out the capital gains tax for their heirs entirely.

This is the core of the debate about who pays taxes in the us. Is it a tax on what you earn, or what you have? Currently, it's almost entirely on what you earn.

Why Some People Get Huge Refunds

You probably know someone who treats their tax refund like a lottery win. "I’m getting $6,000 back!"

This usually happens because of refundable credits. The Earned Income Tax Credit is one of the biggest anti-poverty programs in the country. It’s designed to encourage work by giving money back to low-income earners, especially those with kids. In these cases, the person isn't just paying zero taxes; the government is actually sending them "negative" tax dollars. This is a deliberate policy choice to keep families afloat, but it's often used as a talking point to argue that a large portion of the population doesn't "contribute."

What This Actually Means for You

Understanding who pays taxes in the us isn't just about political trivia. It’s about knowing how to navigate the system so you aren't overpaying. Most people leave money on the table because they don't understand deductions or they're afraid of the IRS.

First, realize that "tax avoidance" is legal; "tax evasion" is a crime. Avoiding taxes means using the rules—like putting money into a 401(k) or a Health Savings Account (HSA)—to lower your taxable income.

Second, if you’re a W-2 employee, check your withholdings. If you get a $5,000 refund, you basically gave the government an interest-free loan all year. You could have had that money in your paycheck to pay down high-interest debt or invest.

Practical Steps to Handle Your Tax Burden

Stop thinking about taxes only in April. By then, it’s too late to change what happened the previous year.

- Max out your HSA if you have a high-deductible plan. It’s the only "triple-tax-advantaged" account. No tax going in, no tax on growth, and no tax coming out for medical expenses.

- Track your business expenses religiously. If you have a side hustle, every mile driven and every portion of your home office counts.

- Understand the "Standard Deduction." For 2024 and 2025, it's quite high. Most people no longer need to itemize things like mortgage interest unless they have a very expensive home or massive charitable donations.

- Keep an eye on legislative changes. Tax laws expire. Many of the provisions from the 2017 tax cuts are set to "sunset" or end in late 2025. If Congress doesn't act, almost everyone's tax rates will jump in 2026.

The US tax code is over 6,000 pages long. Nobody knows all of it. Not even the people at the IRS. But knowing the broad strokes of who is paying—and why—helps you see through the noise. It’s not just about the 1% or the 50%; it’s about a complex, messy system that tries to balance funding a superpower with keeping the economy moving.

Start by looking at your effective tax rate, not just your tax bracket. Your bracket might be 22%, but after deductions, you might only be paying 12% to the feds. That’s the number that actually matters for your lifestyle.

Audit your own finances. Look at your last return. If you see a massive refund, go to the IRS withholding estimator and adjust your W-4 at work. If you see a massive bill, start looking into pre-tax contributions. The system is rigged in favor of those who know the rules, so take the time to learn them.